Negative Gearing and Capital Gains Tax Reform

Supporting home ownership with a fairer and more efficient tax system

The Government is reforming negative gearing and capital gains tax (CGT) arrangements. These reforms will limit the benefits of negative gearing to new residential properties, re-introduce capital gains tax cost base indexation, and introduce a 30 per cent minimum tax on capital gains.

Since 1999, housing prices have risen more than twice as fast as average full time earnings and, since 2001 to 2021, the home ownership rate for households 25 to 34 years old has declined by seven percentage points.

These changes will help level the playing field for first home buyers, preserve the gains investors have made, and support investment in new housing supply.

From 1 July 2027, the Government will:

• limit negative gearing for residential property investments to new builds; and

• replace the 50 per cent CGT discount for individuals, trusts and partnerships with cost base indexation and a 30 per cent minimum tax rate on capital gains.

These changes will rebalance our tax system, allowing the Government to take pressure off wage earners and first home buyers.

The impact of these changes on existing investments will be limited. Properties held before announcement (7:30pm AEST 12 May 2026) will be exempt from the negative gearing changes. The CGT reforms will only apply to gains accruing after 1 July 2027.

Rental losses can only reduce income from residential properties

Under current tax settings, losses from a rental property can be used to reduce other forms of taxable income (e.g. salary and wages). This encourages leveraged property investments that can lead to investors receiving greater tax advantages than those available to owner occupiers.

From 1 July 2027, losses related to existing residential investment properties purchased from 7:30pm AEST 12 May 2026 will only be deductible against other income from residential properties, including capital gains.

However, when an investor has excess losses, they will be able to carry forward that excess to offset residential property income in future years. Enabling losses to be carried forward ensures investors remain able to claim a deduction in the future for costs such as maintenance.

These changes will apply to individuals, partnerships, companies and most trusts. Widely held trusts (for example, most managed investment trusts) and superannuation funds (including SMSFs) will be excluded.

Cost base indexation

The current 50 per cent CGT discount was introduced in 1999, allowing taxpayers to reduce their taxable capital gain by half rather than adjusting for inflation. As a result, the 50 per cent discount does not accurately approximate the inflation component of gains, meaning investors are undercompensated or overcompensated depending on their returns.

Returning to indexation based on the Consumer Price Index (CPI) aligns with the original intent of the CGT regime and supports productivity over time by ensuring that investment decisions are taken for economic reasons, not due to tax outcomes.

Indexation will be calculated using CPI in a similar manner to arrangements previously in place between 1985 and 1999. The ATO will provide guidance and tools to support calculation of this adjustment.

These changes will apply to all CGT assets (including property and shares) held by individuals, partnerships and trusts for at least 12 months. Applying these changes broadly across assets ensures the CGT settings are broadly asset neutral with only targeted exemptions.

Minimum tax on capital gains

A minimum tax rate of 30 per cent will apply to real capital gains accruing from 1 July 2027 (with no impact until the income is realised).

This will not affect people whose capital gains are already taxed at rates of at least 30 per cent. The introduction of the minimum tax reduces the benefit of taxpayers deferring capital gains realisation to years where their marginal tax rates are low. It ensures their gains are subject to a tax rate closer to the rate they faced during their working life and is commensurate with the tax rate paid by most workers.

Recipients of means-tested income support payments, such as the Age Pension or JobSeeker, will be exempted from the minimum tax if they receive any payment in the financial year in which they realise the capital gain.

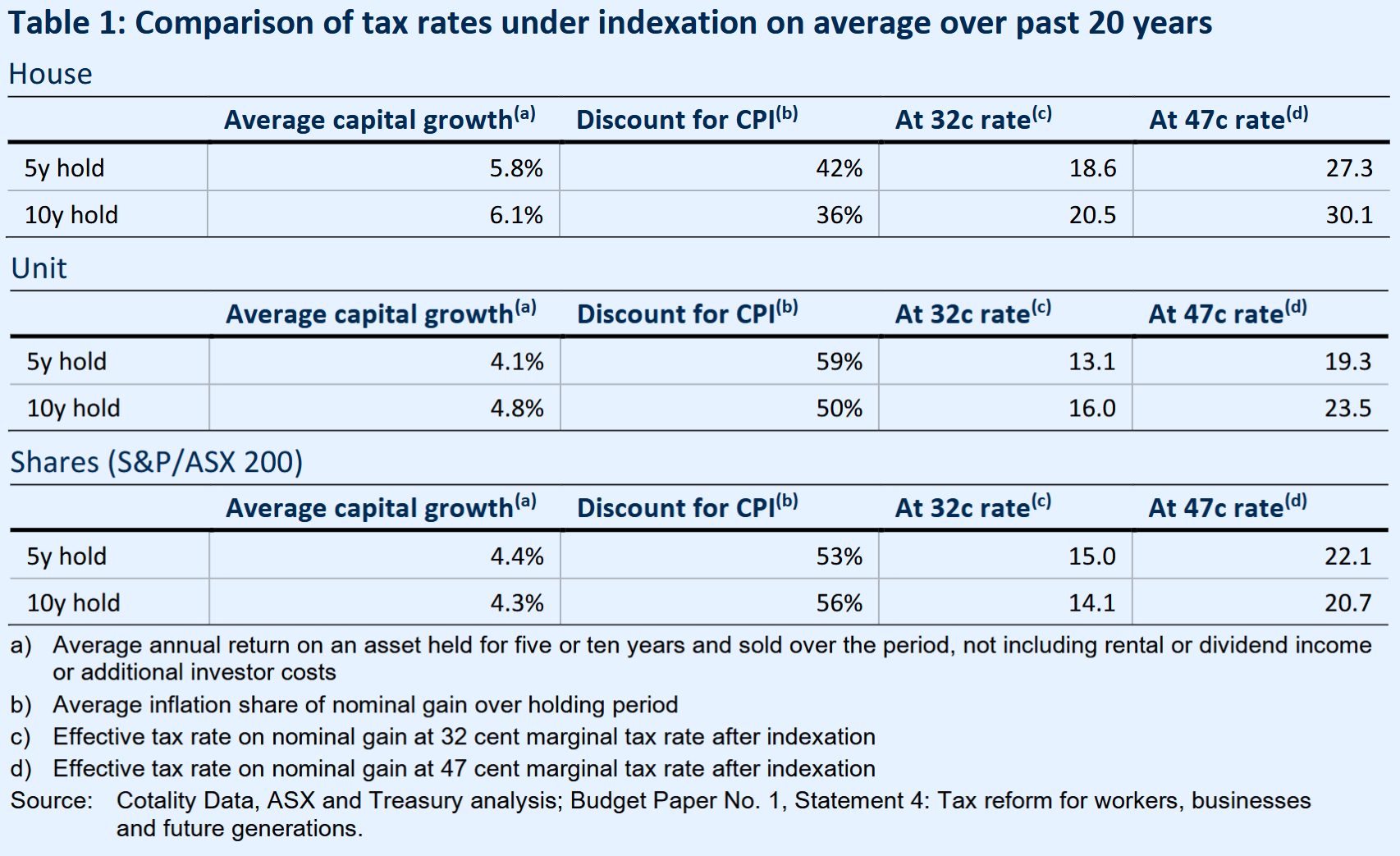

Comparison of Returns, Inflation and Effective Rates

Under these new arrangements, the effective tax rate on nominal capital gains would vary depending on an individual’s marginal rate, their returns and the inflation rate over the period the asset had been held.

As shown below, if indexation had been in place over the past 20 years instead of the current arrangements, the effective discount would have ranged from 35-60 per cent on average for typical assets held for five or ten years.

This equates to an effective tax rate on the nominal gain of between 13 per cent and 30 per cent.

Transitional arrangements

Transitional arrangements for negative gearing

New builds can continue to be negatively geared before and after 1 July 2027.

For established residential properties:

• Properties held at announcement (including where a contract has been entered into, but not yet settled) will be allowed to be negatively geared in future years until sold. This ensures that arrangements for taxpayers who have already made investment decisions based on the existing negative gearing rules will not

change.

• Properties purchased between announcement and 30 June 2027 may be negatively geared during this period, but not from 1 July 2027.

• Properties purchased from 1 July 2027 will not be able to be negatively geared.

Transitional arrangements for capital gains tax

For eligible CGT assets other than new residential properties:

• There will be no changes in arrangements for assets purchased and sold prior to 1 July 2027.

• Assets purchased after 1 July 2027 will be treated wholly under the new arrangements.

• Assets owned prior to 1 July 2027 and sold after 1 July 2027 will be treated under current arrangements on gains made prior to this date, and under the new arrangements for gains made after this date (with no impact until gains are realised).

The 50 per cent CGT discount will apply to the difference between the asset’s cost base and its value at 1 July 2027. Indexation and the minimum tax will be used to calculate the CGT on gains accruing from 1 July 2027 (using the asset’s value at 1 July 2027 as the asset’s cost base).

An asset’s value at 1 July 2027 will be determined by taxpayers as part of their tax return in the year the asset is realised. Taxpayers can either:

• seek a valuation of the asset as at 1 July 2027, which will include using quoted prices for assets such as shares; or

• use a specified apportionment formula that estimates the asset’s value on 1 July 2027, based on its growth rate over the asset’s holding period. The ATO will provide tools to estimate this value for taxpayers.

These transitional arrangements also apply to legacy assets, including those purchased before 1985. Gains on pre-1985 assets accrued before 1 July 2027 will continue to be exempt.

New build exemption

Investors who buy new builds will be able to choose either the 50 per cent CGT discount or indexation and the minimum tax when they sell the property.

These investors will also continue to have access to negative gearing. This means if they make a rental loss on a new build, they can still use that loss to reduce their taxable income (including salary and wages).

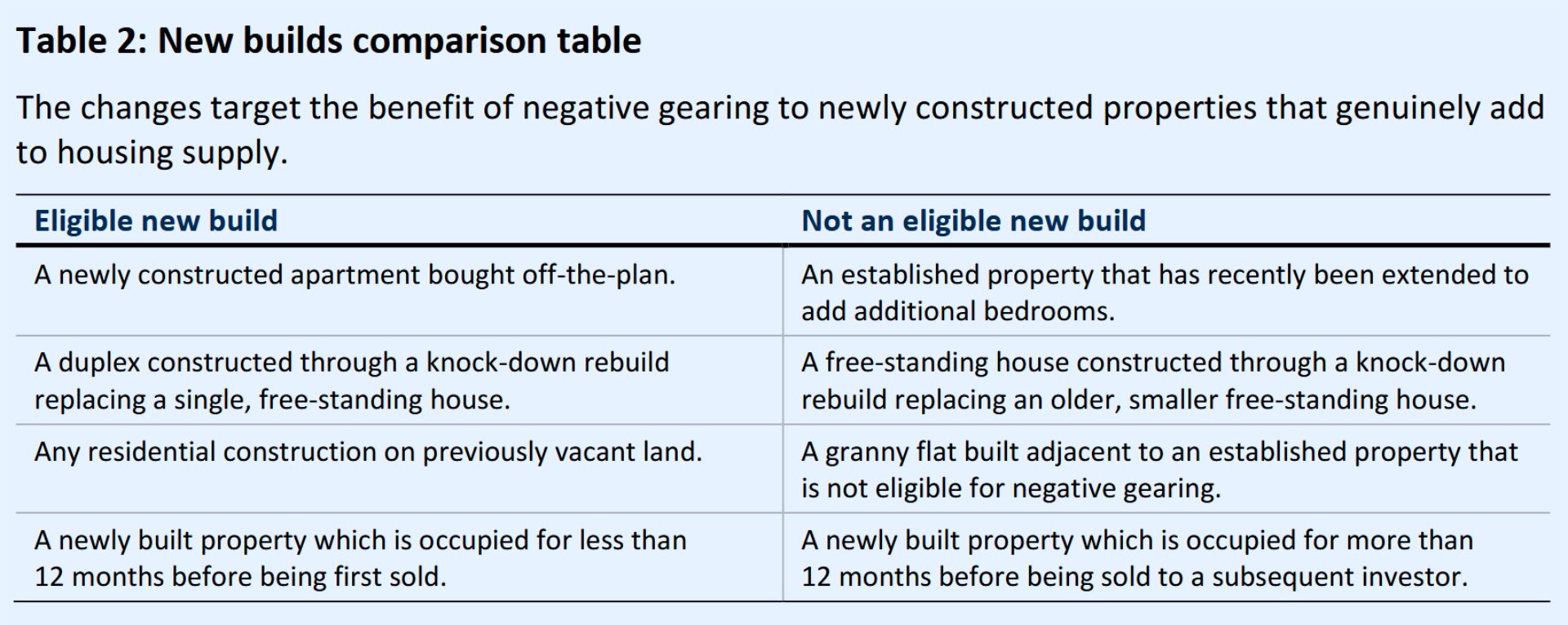

New builds are residential properties which genuinely add to supply (see Table 2). This will include:

• dwellings constructed on vacant land, or

• where existing properties are demolished and replaced with a greater number of dwellings.

Knock-down rebuilds or substantial renovations that do not increase supply will not be eligible. A new build cannot have been previously sold, unless first owned by the builder and not occupied for more than 12 months.

Subsequent purchasers of the dwelling will not be able to access the 50 per cent CGT discount or negative gearing in relation to that property. This is similar to how stamp duty exemptions apply to new builds under some state-based arrangements.

Other exemptions

The main residence will continue to be exempt for CGT purposes. The four small business CGT concessions will also be unchanged.

The existing 60 per cent CGT discount applying to qualifying affordable housing will be fully retained to preserve incentives to invest in those assets.

Given the unique characteristics of the tech and start up sector the Government will consult on the interaction of the capital gains tax reforms and incentives for investment in early-stage and

start-up businesses.

Changes to negative gearing will only apply to residential property. Commercial property and other asset classes, such as shares, will remain subject to existing arrangements.

Further exemptions to the negative gearing changes will also be available for private investors who support government housing programs, for example, through the provision of affordable housing.

Policy impacts

Changes to negative gearing arrangements

Every existing property owner will be able to continue to negatively gear any properties held before the time of announcement (7:30PM AEST on 12 May 2026).

All future investors will still be able to negatively gear property investments if they are new builds. Around 1 per cent of taxfilers acquire negatively geared properties each year. In 2022–23, this was around 230,000 individuals.

Changes to capital gains tax arrangements

The new arrangements will only apply to capital gains that accrue after 1 July 2027 when they are realised. Individuals may pay more or less tax than under current settings depending on investment returns (see Cameos: Different rates of return).

Around 7 per cent of taxfilers report a net capital gain each year. In 2022–23, this was around 1.1 million individuals. Most of these taxfilers used the CGT discount (which is only available for assets held for more than 12 months).

Market impacts

The transitional arrangements minimise risks of asset market disruption. Properties held at announcement (including where a contract has been entered into, but not yet settled) will be allowed to be negatively geared in future years, meaning there will be no incentive to buy or sell properties before specific dates.

Only capital gains accrued after the commencement of the policy will be subject to new arrangements, meaning there is no incentive to buy or sell assets before this date.

Housing impacts

These changes will support more first home buyers to enter the housing market over time, and form part of a package of reforms that will support supply overall.

Treasury modelling suggests that the reforms will increase the owner occupier share of the housing market, resulting in around 75,000 additional owner-occupiers over the next decade. This is equivalent to reversing around 10 years of declines in the home ownership rate.

The reduction in investor demand is expected to lead to a small and temporary slowing in house price growth, estimated to see prices grow by around 2 per cent less over a couple years relative to no tax policy change. Lower house price growth will have a small impact on housing supply, more than offset by the additional homes supported by housing supply measures in the Budget.

The reforms are likely to have a small impact on rents, with an expected increase of less than $2 per week for a household paying the current median rent. The combination of the Government’s policies in this Budget will add to housing supply, which will exert downward pressure on rents over time. The Government’s increases to Commonwealth Rent Assistance in 2023 and 2024 total more than $20 per week for a single person receiving the maximum rate, and renters can also benefit from the Government’s tax cuts.

International comparisons

In its most recent country report on Australia, the OECD recommended cutting or eliminating the capital gains tax discount and phasing out negative gearing to improve Australia’s tax system.

Countries tax capital gains and treat rental deductions in a range of different ways, so direct comparisons depend on specific circumstances. In particular, headline tax rates applying to nominal and real gains are not directly comparable.

The effective tax rate on nominal gains in Australia under the new indexation arrangements will depend on the nominal return, inflation and marginal tax rate. As highlighted above, over the past 20 years nominal tax rates on average returns could have been in the order of 20 to 30 per cent for someone on the top marginal tax rate, though in some cases the effective rate could be higher where real returns are large.

While there are difficulties in comparing tax arrangements across jurisdictions, similar rates apply across many OECD countries.

Cameos

Impacts on existing property investors

Michael owns an investment property purchased before 12 May 2026 that is negatively geared. He can continue to negatively gear this property in future years by using losses from his investment property against other income.

Michael sells the property two years after the policy commences for $560,000. Michael still receives the 50 per cent CGT discount for the capital gain he makes on the property between the purchase date and 1 July 2027. He uses ATO tools to determine its value on that date was $500,000. After adjusting for two years of inflation of 2.5 per cent, his taxable capital gain for the period after 1 July 2027 is $34,688, slightly more than if he had applied a 50 per cent discount (which would have resulted in a taxable capital gain of $30,000). Assuming a 47 per cent tax rate, the tax on his gain since 1 July 2027 is $16,303 (instead of $14,100 with a 50 per cent discount). Michael does not pay any tax on the capital gain until he sells his property.

Carrying forward losses for future property investors

A person buying a new build property can continue to negatively gear as per current arrangements.

For an individual purchasing an existing property after the announcement, the impact depends on the size of their rental loss and how much other income they have. For example, assuming a rental loss of $14,810: 1

• For a person with $80,000 in other income this deduction would be worth $4,761.

• For a person with $210,000 in other income this deduction would be worth $6,961.

This person will instead carry forward their $14,810 loss to use against future property income. The tax value of this future deduction will also depend on their other income at the time.

Negative gearing an existing residential property bought after announcement

Yoonseo earns an income of $100,000 and buys an existing residential investment property for $519,000 (including stamp duty) after the policy start date, rents it out and sells it ten years later for $814,447. Over the first five years that she owns the property she has net rental losses andaccumulates $22,879 of carry forward losses.

In the following five years, Yoonseo applies most of these carried forward losses to reduce her positive net rent over this period from $18,079 to zero. In the year she sells the property she uses the remaining carried forward losses to reduce her real estate capital gain from $150,083 to $145,284. Overall, she pays $186 more in nominal tax over the years of her investment compared to previous settings.

Had Yoonseo bought a new build property, she would not pay additional tax as negative gearing and the existing capital gains tax discount would still be available for this property.

Cost base indexation

Zoe purchases shares in a company for $100 on 1 July 2027. She then sells her shares on 1 July 2032 for $125, having made a nominal gain of from this investment of $25, with an investment return of 4.6 per cent per year.

As the shares were purchased after 1 July 2027, Zoe’s capital gains are subject to cost base indexation. Inflation is 2.5 per cent each year Zoe holds the assets and, using ATO tools, Zoe can work out that the indexed cost base of the shares is $113. Zoe’s taxable capital gain is reduced from $25 to $12 under cost base indexation. This is slightly less than the taxable capital gain of about $13 under the 50 per cent discount, meaning she will pay slightly less tax.

Transitional CGT arrangements

Jane purchases an asset on 1 July 2022 for $800,000. She sells the asset on 1 July 2032 for $1,600,000 earning a 7.2 per cent annual return. Using ATO tools, Jane determines that the asset was worth $1,131,371 at commencement of the policy (1 July 2027). Under the transitional rules, Jane calculates her taxable capital gain by adding:

• Taxable capital gains of $165,685 earned before commencement, which is equal to gross capital gains of $331,371 with the 50 per cent CGT discount; plus

• Taxable gains of $319,958 earned after commencement, which is equal to the gain of $468,629 less cost base indexation.

Her total taxable capital gain is $485,643. This is more than the $400,000 that would have been calculated if a 50 per cent discount applied to the gain overall. Assuming a 47 per cent tax rate, the tax on her gain is $228,252 (compared to $188,000 with a 50 per cent discount).

Different rates of return

People will be affected differently depending on the rate of return on their assets. For example, assuming 2.5 per cent inflation, an asset purchased for $500,000 in July 2027, a holding period of 10 years, and $100,000 in other income per year:

• David earns an annual rate of return of 5 per cent, similar to longer term returns on residential real estate. He will have a taxable capital gain of $174,405 under cost base indexation compared to $157,224 under the current 50 per cent discount. He will pay an extra $8,075 in tax due to the reforms.

• Ben earns a lower 2.5 per cent annual return. As Ben does not earn a positive return on his investment after inflation, he will not have a taxable capital gain under cost base indexation. Under the 50 per cent discount his taxable capital gain would have been $70,021. He will pay $24,858 less in tax due to the reforms.

• Kate earns a higher 7.5 per cent annual return. She will have a taxable capital gain of $390,474 under cost base indexation compared to $265,258 under the current 50 per cent discount. She will pay an extra $58,851 in tax due to the reforms. Minimum tax on capital gains Jack has a taxable income before capital gains of $25,000 in 2029–30 and realises a capital gain of $10,000 on an asset that he purchased in 2027–28. Jack does not receive an income support payment so is not exempt from the minimum tax.

• The tax on Jack’s capital gain of $10,000 is $1,400, or a tax rate of 14 per cent (excluding the Medicare levy). As this is lower than 30 per cent, Jack pays an additional $1,600 in tax to bring the tax rate on his capital gain up to 30 per cent. Jack may have tax offsets available to reduce the minimum tax and would be exempt from the minimum tax if he received an income support payment in that year.